I’ve done some more work to test the RS model, though still more needs to be done. However, since I am using this to manage my leverage, it sort of fulfills my purpose.

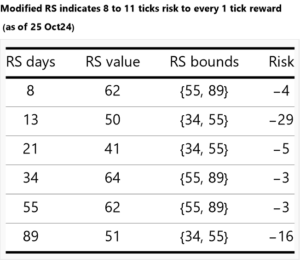

I have been doing some risk reward work. Specifically, I have been trying to analyse the distribution of forward returns for a particular forward time window. The question I ask is: “if the signal is within the bracket shown, what were the historical losses?” The table then shows the risk scaled against 1 tick of reward during the period. The line at the top represents a weighted average with two different weighting schemes: 1) duration of modified signal; and 2) length of window.

I’ve titled the table to show me what I should be ready to accept. In this particular case, as of 25 October, I should be ready to accept 11 ticks in losses for each 1 tick in reward. This is not a terribly exciting risk-reward ratio – and I have left out the typical size of rewards in the intervals.

The next analysis will dive into the probability of reward vs loss.