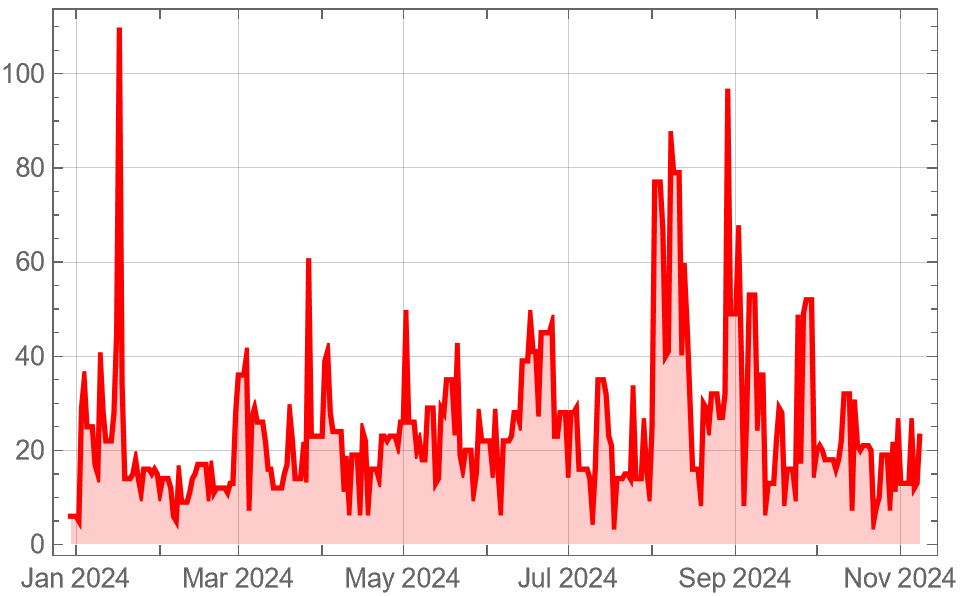

I created a backtest routine 2 weeks ago. This is what the (trader) momentum signal looks like over time. To the naked eye, if the signal is above 40, I am feeling comfortable adding exposure. Once it falls below 20, it seems a leveraged position is best avoided.

I am performing a series of tests to see the usefulness of the 40 and 20 levels. Both levels are likely to depend upon volatility regimes, perhaps I should let these levels also be determined algorithmically. That would be a 2 stage algorithm. Calculating the trader signal is the 1st stage of the algorithm.

The signal through 2024 looks like this. I think it replicates what I have experienced quite level, but I will look to model performance on the basis of the signal next.